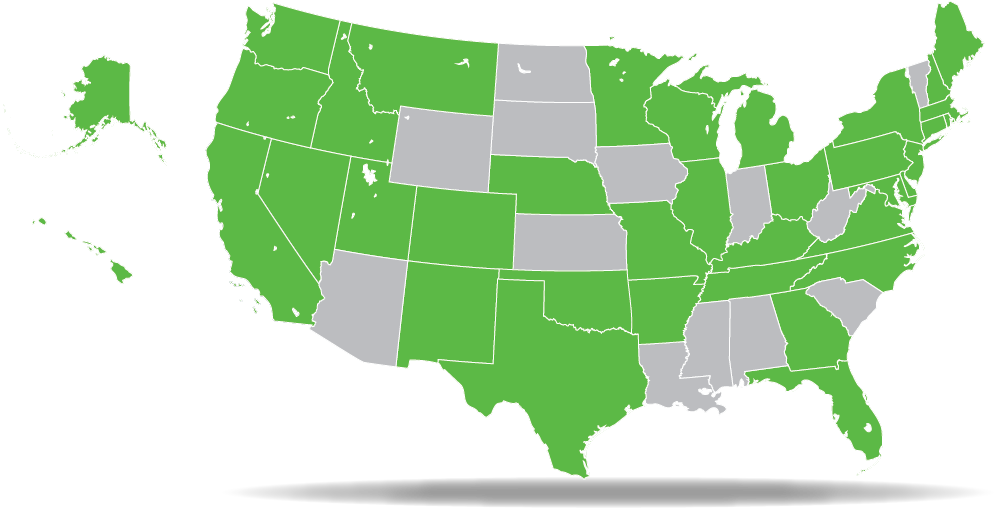

Over the past several years, Commercial Property Assessed Clean Energy (C-PACE) has quietly moved from a niche tool to a mainstream part of the commercial real estate capital stack. C-PACE programs are now active or in development in 40 states plus Washington, D.C., with new or updated legislation in places like Georgia, New Mexico, New Jersey, North Carolina, Idaho, and New York.

Cumulative C-PACE originations have surged past $10 billion nationally, with 2026 expecting to deliver record volumes and continued double-digit year-over-year growth as more owners, lenders, and institutional investors embrace the structure.

This growth has been happening despite a variety of industry changes — from fluctuating interest rates to tighter bank lending to rigorous new local building codes. C-PACE’s fixed-rate, non-recourse financing, repaid through a special property tax assessment and typically transferable to future owners, has become a consistent and attractive way to fill capital gaps, reduce weighted average cost of capital, and make projects pencil that might otherwise stall.

Get some details about C-PACE by reviewing the commonly asked questions below.

Q: C-PACE financing is becoming a go-to source of capital for borrowers. What are some of the factors that have driven this, in terms of both current finance market conditions and the value proposition of C-PACE?

Three big factors are driving the growth of C-PACE right now. First, there’s a healthy amount of real estate activity in the market, but banks are facing more scrutiny from regulators. That’s leading many bank lenders to either reduce leverage or shorten their loan terms, which can make projects harder to finance.

Second, interest rates are playing a huge role. No matter where rates are, C-PACE financing offers access to long-term, low-cost capital. The fact that it’s long-term financing at a very competitive fixed rate really adds to its appeal. The ability for a project to lock in low-cost rates for 20-30 years without refinance risk gives a lot of project owners the stability they are looking for. Having said that, C-PACE also works as a short- and medium-term option, offering the flexibility many developers need to cover lease-up or bridge to other long-term options.

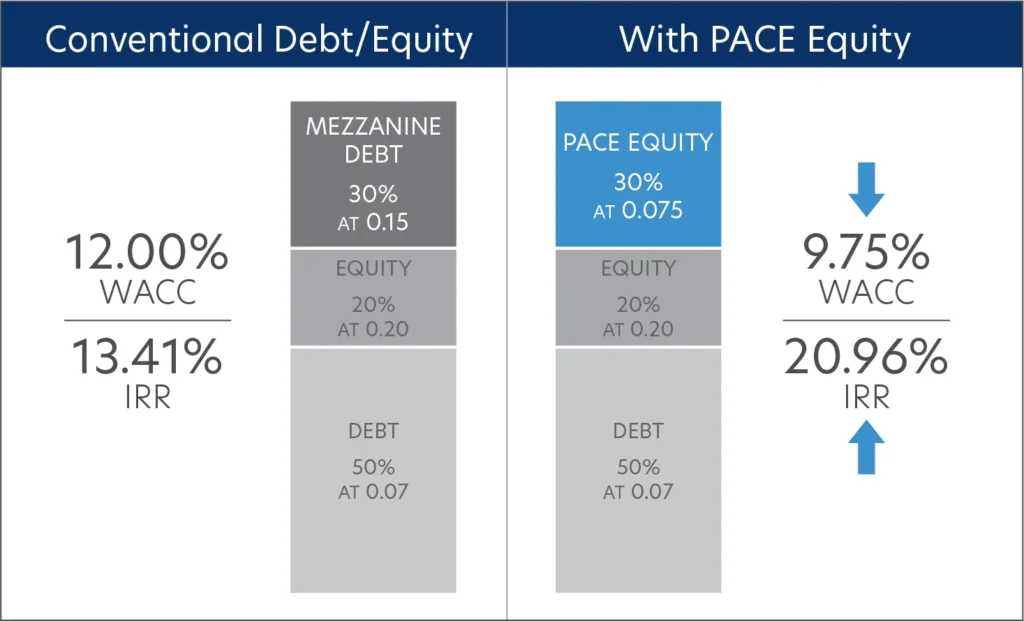

When rates go up, equity investors expect higher returns. By using C-PACE in place of preferred equity, or mezzanine debt, you can bring down the overall cost of capital on a project and boost returns.

Third and finally, the growing awareness and utilization of C-PACE recapitalizations has become a driving force. As the ability to recapitalize a project using C-PACE has grown, more developers have utilized recap in significant ways. From covering cost overruns, funding interest reserves, to reshuffling a capital stack, developers and sponsors have found C-PACE to be a flexible tool that goes beyond development projects alone.

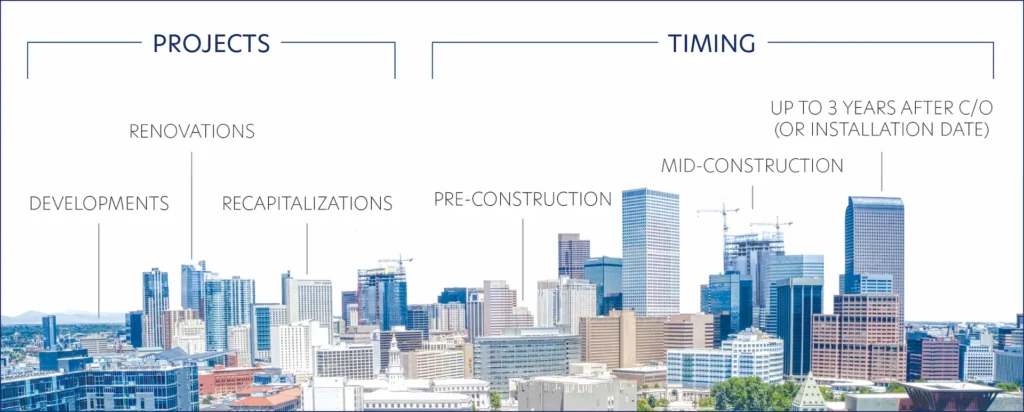

Q: One of the hallmarks of C-PACE is its versatility. While it can help make development and renovation projects pencil out, it has also become a vehicle for refinancing existing properties. How is a refi via C-PACE structured?

C-PACE isn’t just for new construction or renovation projects anymore. While it’s always been a great way to fund a construction project, we’re now seeing more refinance deals.

There are a lot of ways to structure a C-PACE refi. We’ve used it to partially pay down senior debt and restructure the capital stack, fund interest reserves, help properties reach stabilization, and cover cost overruns.

One of the most common uses for C-PACE has been refinancing with the goal of extending a loan to allow more time for a project to reach stabilization. In this scenario, developers can refinance a portion of senior debt, or, in some cases, all of the senior debt with C-PACE financing. Using C-PACE in this way allows for a pending maturity on a still stabilizing property to become less of an issue with more breathing room for lease up to stabilization.

Q: While C-PACE has increased its visibility among borrowers, it is also growing in acceptance among senior lenders. What has influenced their thinking?

Senior lenders are definitely more accepting of C-PACE, with over 400 banks already having provided consent to C-PACE in the stack. In the big picture, it’s still a young product compared to traditional mortgages that have been around for centuries.

With that said, as C-PACE has grown, senior lenders have switched from being skeptical of C-PACE to seeing it as an asset to get deals done. Senior lenders see C-PACE as an accretive tool to help them win deals and differentiate themselves. Additionally, many senior lenders have started viewing C-PACE as a way to assist and grow their book of business. Perhaps a deal is too large for a senior lender to do alone, or the deal needs some additional funding to get completed – many senior lenders are turning to C-PACE to get deals done, thus supporting their important relationships. If you are a lender, PACE Equity Finance has a lender partnership program that fuels our Total Debt Solution offering.

Q: What’s behind the growing momentum with larger C-PACE assets?

The growth in the number of C-PACE funded projects is growing along with the average funding size. This growth is tied to the same trend we’re seeing with lender acceptance—more people understand what C-PACE can do.

C-PACE is a powerful financing tool that works just as well for big, complex projects as it does for smaller ones. The core features of C-PACE, such as its fixed rate, lower cost of capital, and non-recourse features, makes sense for large projects. As a balance sheet lender backed by a $26+ billion balance sheet, we have the ability to fund deals of any size.